Bank of the Generation! SWIFT CODE: GOBTETAA

Menu

Menu

Corporate Governance

Risk Management Philosophy and Approach

The banking industry is characterized by deepening of financial products and services as well as rapid changes in the business and regulatory environments. So along with this endeavor come the inevitable, more complex, interrelated and wide range of risks that are inherent to the banking products and services.

However, if these risks are not properly managed; they can bring about an adverse impact on our operations, reputations, use of human resources as well as financial performance. Hence, with a view to minimize the uncertainty witnessed in the course of implementing our business strategy; the Bank is identifying and controlling risks while maximizing opportunities that allow the attainment of the Bank’s goals and objectives.

In order to ensure the effective management of risks, GBB has crafted a comprehensive risk management framework which has secured green light from the Board. This risk management framework deals with the governance structure for managing risks, our risk philosophy, risk appetite and tolerance levels, as well as our risk management approach. Accordingly, our risk assessment and mitigation strategy is aligned with the Bank’s strategy and is an integral part of the annual business plan.

Risk Philosophy

Effective risk management is not about eliminating risk taking, which is indeed a fundamental driving force in business. It is rather strengthening risk management practices. Goh Betoch Bank has defined its risk management philosophy where in it sets out how risk is considered in its business activities, how risk management components are applied, including how risks are identified, the kinds of risks accepted and how they are managed.

The Bank fosters calculated and responsible risk taking culture that takes into account risks and rewards inherent in all of its business activities. Risk appetite is the aggregate level and types of risk that the bank is willing to assume or to avoid, in pursuit of its goals and objectives. We assume risks that are considered prudent and within our risk appetitive. It is determined by considering the relationship between risk and return while considering that of the Bank’s capital, internal controls and other requirements.

GBB’s risk philosophy and risk management approach is based on the principles of risk taking culture that promote awareness, ownership and proactive management of risks and strong corporate governance that clearly defines risk taking responsibility and authority along with accountability for risk taking.

Risk Governance

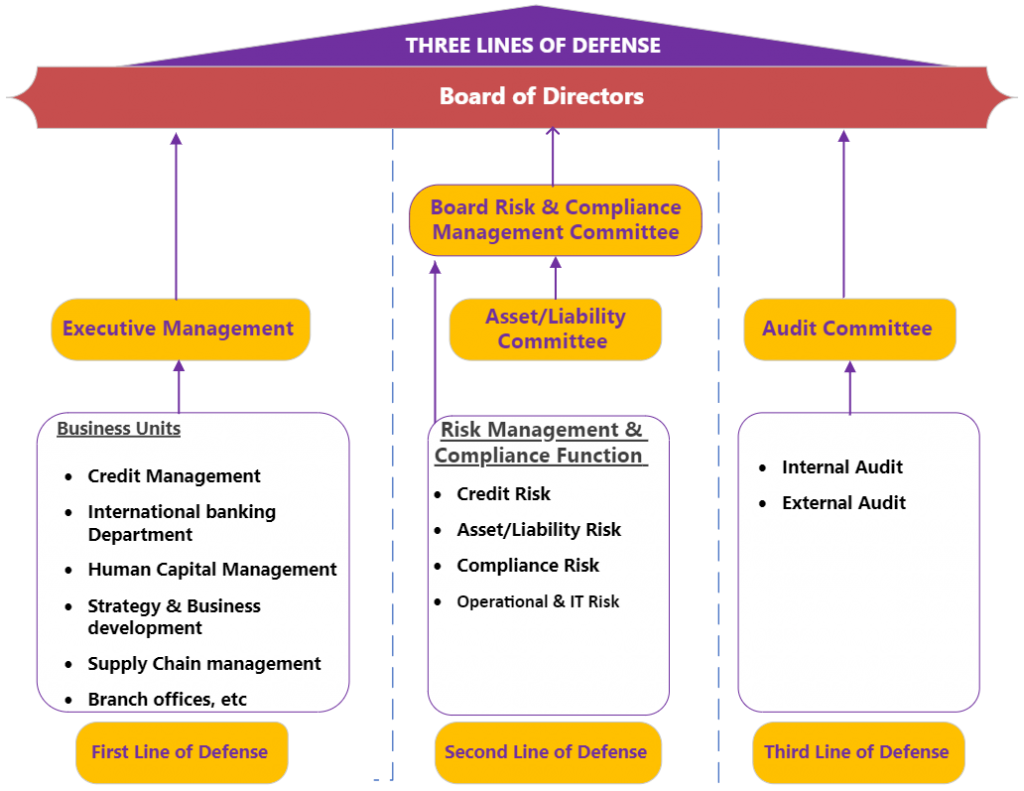

In our Bank, risk governance is the architecture within which risk management operates. It is through this channel GBB undertakes risk management work, provides guidance for sound and informed decision-making and efficient allocation of the Bank’s resources. Hence, our Bank’s risk governance underlines the need for joint efforts of both the Board and management towards effective management of risk. It is for this reason that the Bank has adopted the “Three Lines of Defense” model.

THE BOARD OF DIRECTORS

- Establishes risk management framework and approach for risk governance;

- Sets appropriate tone at the top;

- Sets risk appetite or risk tolerance;

- Undertakes oversight of risk management systems and internal controls; and

Reviews identified risks and mitigation plans and monitors risk exposure.

THE BOARD OF DIRECTORS

- Reviews and recommends risk strategy, policies and risk appetite or tolerance;

- upervises proper implementation and monitoring of internal controls;

- Reviews adequacy and effectiveness of the Bank’s management framework; and

- Monitors the proper implementation of risk mitigation plans.

THE BOARD OF DIRECTORS

- Reviews adequacy and effectiveness of the Bank’s internal control framework;

- Oversees financial reporting risks; and

- Oversees internal and external audit processes.

MANAGEMENT

- Implements risk management practices within all the business units and functions;

- Supports the Board and Risk Committee with regards to risk governance and oversight;

- Ensures the alignment of risk management and monitoring with the

- Bank’s philosophy, appetite and tolerance;

Go through the risk assessment report and takes corrective actions timely; - Reviews and assesses the adequacy of the Bank’s risk management systems and tools; and

- Reviews efficiency and effectiveness of mitigation schemes and coverage of risk exposures.

Risk Management Process

Goh Betoch Bank puts in place a systematic risk review process so as to identify, monitor, manage and report risks that the Bank has faced in it operation in line with its risk philosophy. In this regard, it is clearly stated that the Management has primary responsibility of identifying, managing and reporting key risks the bank has faced. The Management is also in charge of ensuring that the risk management framework is effectively implemented among all the business units.

Then the Risk and Compliance Management Function facilitates the identification and measure of key risks and report risk monitoring outcomes to the Board’s Risk Committee. Moreover, scenario/stress testing, business continuity/disaster recovery management and crisis management are also incorporated in the bank’s risk management endeavor.

The Risk Management Function undertakes regular monitoring work with a view to ensure that the Bank’s risk profile is in accordance with the predefined risk appetite or limit. In addition, ongoing assessment would also be executed with regards to the effectiveness of risk management and controls. Apart from this, independent assessment and reviews are also conducted by internal auditors to ensure the relevance of the Bank’s risk management framework and the results are reported to the Board.

External auditors also review our internal controls and any non-compliance and internal control weaknesses, together with their recommendations, are reported to our bank. Subsequently, the Management, on its part, takes corrective actions to address the external auditors’ recommendations.

As a financial institution, GBB is expected to be vulnerable to the following risks:

- Credit risk: It is the potential that the bank borrower or counterparty fails to meet its obligations in line with the agreed terms.

- Liquidity risk: this is a risk when the bank cannot meet payment obligations timely and in a cost effective manner.

- Market risk: It is the potential that changes in the market rates/process may have an adverse impact on the bank’s financial situation. In other words, it is the risk that the bank’s earnings or capital position will be affected by interest rate and foreign exchange rate fluctuations.

- Operational risk: this is a risk of loss arising from inadequate or failed internal processes, people and systems or from external events.

Money Laundering and Financing of Terrorism (ML/FT) Risk Management

Vulnerability to the risk of money laundering and terrorism financing nowadays has increased globally and demands the attention it deserves. If not properly managed and contained, Money Laundering (ML) and Terrorist Financing (TF) risk poses serious impact on the Bank’s finance and institutional reputation. Hence, being cognizant of the pivotal role of effective management of ML/TF risk, GBB has put in place AML/CFT program that comprises AML/CFT/CFP policy, procedure, ML/TF risk assessment, employees’ due diligence, Know Your Customer (KYC)/Customer Due Diligence (CDD), employees’ training and monitoring and reporting. Moreover, to ensure its adequacy; internal and external auditors also undertake independent testing.